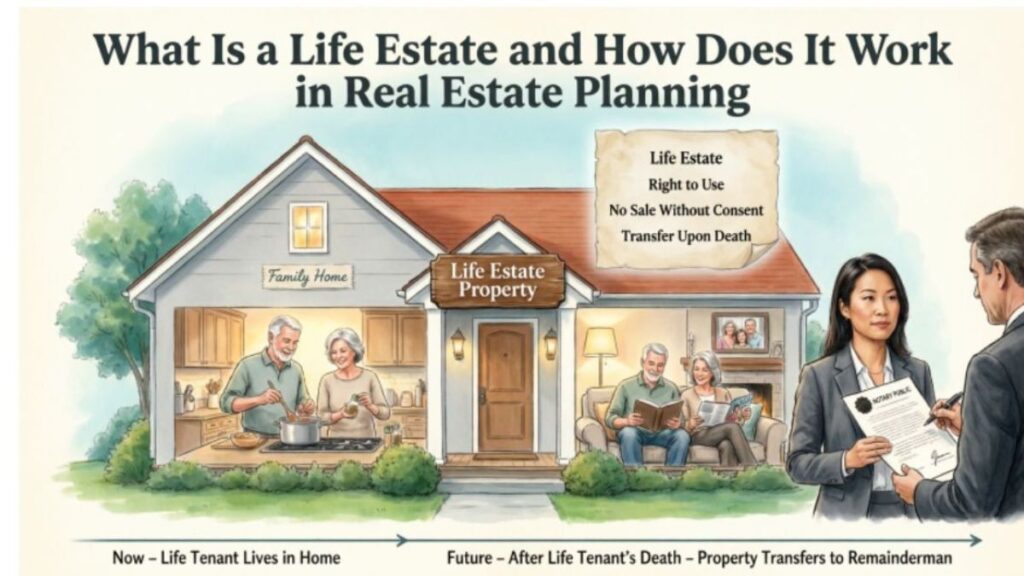

A life estate is one of the most practical tools used in modern estate planning strategies. It allows you to continue living in your home while legally preparing for future ownership transfer. Many families use this approach to simplify real estate inheritance planning and reduce complications later.

Unlike traditional inheritance methods, a life estat’e creates a structured legal ownership arrangement between two parties. This setup helps ensure automatic property transfer while supporting long-term financial planning and legacy planning goals.

What Is a Life Estate?

At its core, what is a life estate refers to a legal agreement that divides property ownership across different time periods. One person keeps lifetime property rights while another gains future ownership.

This structure supports asset transfer planning by ensuring the property passes directly to a chosen beneficiary without probate. It’s commonly used in family homes and retirement estate planning.

Simple Definition of a Life Estate

A life estate allows a homeowner to live in and use their property for life. After their passing, ownership automatically transfers to another individual known as the remainderman.

Think of it like lending someone future ownership while keeping present control. This makes inheritance planning predictable and legally secure.

Why Life Estates Are Important in Estate Planning

Estate planning isn’t just for wealthy families. Anyone who owns property benefits from having a clear plan for property succession planning. A life estate helps avoid uncertainty by defining ownership both now and in the future.

For example, parents often want their children to inherit a home without probate delays. Using probate avoidance methods like a life estat’e protects family estate management while reducing estate planning risks.

Overview of Property Ownership Transfer Methods

Property can transfer through wills, trusts, or joint ownership structures. However, many of these options involve court supervision or legal costs after death. That’s why homeowners explore alternatives focused on transferring home ownership after death smoothly.

A life estate stands out because ownership transitions automatically. This makes it attractive for estate planning for homeowners seeking clarity and simplicity.

How Life Estate Ownership Is Structured

Ownership is divided into two interests: current use and future possession. The life tenant holds lifetime usage rights while remainderman ownership activates later.

This real estate legal structure ensures property transfer after death occurs without additional court involvement. It also strengthens wealth transfer strategy planning within families.

Key Parties Involved in a Life Estate

Every life estate includes clearly defined participants. Understanding their roles prevents confusion and supports inheritance disputes prevention. Both parties share ownership interests, though their rights apply at different times.

Who Is the Life Tenant?

The life tenant is typically the original homeowner. They retain life tenant rights including living in the home, maintaining it, or renting it out during their lifetime. They also carry responsibilities such as property tax responsibility, insurance payments, and upkeep. These obligations protect the future value of the property.

Who Is the Remainderman?

The remainderman is the future owner of the property. Although they don’t control daily decisions initially, their legal interest already exists. Once the life tenant passes away, ownership transfers instantly. This automatic property transfer eliminates delays and supports estate distribution planning.

How a Life Estate Works in Real Estate Planning

A life estate functions as a bridge between present ownership and future inheritance. It combines legal certainty with practical housing security. Many families use this model when exploring what is a life estate in estate planning because it simplifies long-term property succession.

Creating a Life Estate Deed

The process begins by drafting a life estate deed. This document legally names the life tenant and remainderman while defining ownership terms. A fiduciary financial advisor or estate attorney often helps ensure compliance with property inheritance laws and local regulations.

Property Rights During the Life Tenant’s Lifetime

During their lifetime, the life tenant maintains control of daily property use. They may live there, make improvements, or generate rental income. However, property control limitations exist. Selling or refinancing typically requires consent from the remainderman due to shared ownership.

Transfer of Ownership After Death

Upon death, ownership passes automatically to the remainderman. No probate court approval is required. This process answers a common question about how to avoid probate with property while preserving family harmony.

Types of Life Estates

Not all life estates function the same way. Different structures offer varying levels of flexibility depending on estate planning needs. Choosing the right type depends on financial goals and asset protection strategies.

Traditional Life Estate

A traditional life estate permanently divides ownership once created. The life tenant cannot sell or mortgage the property independently. While effective for legacy planning, it may limit flexibility if financial circumstances change later.

Enhanced Life Estate (Lady Bird Deed)

An enhanced life estate, often called a Lady Bird Deed, allows the life tenant greater control. They may sell or refinance without beneficiary approval. This version is often preferred for Medicaid planning strategies and long-term care asset protection planning.

Rights and Responsibilities of a Life Tenant

Owning property through a life estate comes with both privileges and duties. Understanding these responsibilities prevents disputes later. Proper management protects both current enjoyment and future ownership value.

Maintenance and Property Taxes

Life tenants must maintain the home and handle ongoing expenses. These include repairs, insurance, and taxes. Failure to meet these duties could impact the remainderman’s future interest and create estate planning risks.

Selling or Renting the Property

A life tenant may rent the property and receive income from it. However, selling usually requires agreement from all ownership parties. This balance protects remainderman ownership while preserving lifetime housing security.

Rights of the Remainderman

Although future owners don’t live in the property initially, they still hold important legal protections. Their role ensures long-term continuity within family estate management plans.

Future Ownership Rights

The remainderman gains full ownership after the life tenant’s death. This includes the right to live in, sell, or lease the property. Because of the step-up in basis rule, beneficiaries may also receive estate tax advantages.

Consent Requirements for Property Decisions

Major financial decisions often require mutual approval. This prevents unauthorized actions that could reduce property value. Such safeguards support balanced joint property ownership planning.

Benefits of a Life Estate in Estate Planning

The benefits of creating a life estate extend beyond inheritance simplicity. It offers emotional reassurance and financial efficiency. Families gain clarity while maintaining housing stability.

Avoiding Probate

One of the biggest advantages is probate avoidance. Property transfers directly without court supervision. This saves time, reduces legal costs, and protects heirs from administrative delays.

Lifetime Housing Security

A life estate guarantees that you can remain in your home for life. Even after naming heirs, your residency rights remain secure. This feature supports retirement estate planning and elder care financial planning.

Simplified Inheritance Process

Because ownership transfers automatically, heirs face fewer legal hurdles. Family conflict risks also decrease. This streamlined approach strengthens legacy planning outcomes.

Disadvantages and Risks of Life Estates

Despite advantages, life estates aren’t perfect. Understanding limitations helps avoid future complications. Every estate planning decision should balance benefits and risks.

Limited Flexibility

Once established, changing ownership terms can be difficult. Property decisions may require cooperation from all parties. These life estate disadvantages can create challenges during financial emergencies.

Potential Family Conflicts

Disagreements may arise over maintenance or property use. Clear communication is essential for inheritance disputes prevention. Careful planning reduces misunderstandings between generations.

Financial and Legal Risks

Life estates may affect eligibility for certain programs. Medicaid eligibility rules can vary significantly. Always evaluate estate planning risks before finalizing arrangements.

Tax Implications of a Life Estate

Taxes play an important role when evaluating ownership decisions. Understanding implications helps prevent surprises later. Proper planning supports capital gains tax planning goals.

Capital Gains Tax Considerations

Beneficiaries often receive favorable tax treatment through a stepped-up property value. This may reduce taxes when selling inherited property. This advantage makes life estates appealing for wealth transfer strategy planning.

Property Tax Responsibilities

The life tenant typically remains responsible for property taxes. Maintaining payments protects ownership continuity. Tax obligations should always be reviewed within long-term financial planning discussions.

Life Estate vs. Other Estate Planning Tools

Many homeowners compare life estates with alternative planning tools. Each option serves different needs. Understanding these differences helps you choose wisely.

Life Estate vs. Will

A will distributes assets only after probate. That process may delay inheritance and increase costs. A life estate bypasses court involvement entirely, offering faster estate distribution.

Life Estate vs. Living Trust

When comparing life estate vs living trust, flexibility becomes the main difference. Trusts allow broader asset management. However, life estates remain simpler and often cheaper for single-property planning.

Understanding a Life Estate

A life estate is a legal ownership arrangement that allows one person to live in and use a property for the rest of their life while another person holds future ownership rights. This setup is often used in estate planning to ensure smooth property transfer after death without going through probate. It creates a clear timeline of ownership, giving the life tenant present control and the remainderman automatic ownership later.

Many homeowners choose a life estate to protect family property and simplify inheritance planning. It allows you to remain in your home while legally preparing for the future transfer of assets. This structure can also support long-term financial planning by reducing legal complications and ensuring your wishes are followed after your lifetime.

Duties and Responsibilities of a Life Tenant

A life tenant has the right to live in and benefit from the property, but those rights come with important responsibilities. They must maintain the home, pay property taxes, handle insurance costs, and complete necessary repairs to preserve the property’s value. Proper upkeep ensures the home remains in good condition for the future owner.

In addition, the life tenant must avoid actions that could reduce the property’s worth, such as neglecting maintenance or making damaging changes. Major decisions like selling or mortgaging the property usually require agreement from the remainderman. By fulfilling these duties responsibly, the life tenant helps protect both their lifetime housing security and the future ownership interests involved.

When Should You Use a Life Estate?

A life estate works best in specific family and financial situations. Timing and goals matter greatly.

Evaluating personal needs ensures better outcomes.

Ideal Situations for Families

Families wanting guaranteed property succession often benefit most. It works well when parents plan to leave a home to children. It’s also useful for nursing home planning and life estate for Medicaid eligibility strategies.

When a Life Estate May Not Be Suitable

If flexibility or future selling plans are uncertain, other tools may work better. Business properties or complex estates often require trusts.

Conclusion

A life estate can be an effective solution if your goal is smooth inheritance and lifetime housing security. It blends legal protection with practical estate planning, making property succession easier for families.

Still, every situation is different. Reviewing your financial goals, family dynamics, and long-term plans ensures you choose the best path forward for protecting your home and legacy.

FAQs

What is a life estate in simple terms?

It’s a legal arrangement allowing someone to live in a property for life while naming a future owner.

Does a life estate avoid probate?

Yes, ownership transfers automatically to the remainderman without court involvement.

Can a life tenant sell the property?

Usually only with the remainderman’s consent unless using an enhanced life estate.

Is a life estate good for Medicaid planning?

It can help with Medicaid planning strategies depending on timing and local regulations.

Who pays property taxes in a life estate?

The life tenant typically handles taxes, maintenance, and insurance costs.